High Touch + High Tech

The personal touch of live advisors with a modern and mobile experience.

Learn More

AB401k is featured in Chapter 4 of Tony Robbins' #1 bestseller UNSHAKEABLE

![]() Attention employees! If you want to tell your employer to uncover the fees of your company's plan, CLICK HERE

Attention employees! If you want to tell your employer to uncover the fees of your company's plan, CLICK HERE

7 minutes or less on our web based form gets the ball rolling

Your dedicated rep will request your current plan document and census. We will send the termination letters to your existing provider

We do the heavy lifting of your transition over 5-6 weeks while you stay entirely focused on your business

You've got a $5 trillion 401(k) industry charging excessive fees to investors simply because no one's rocking the boat or trying to compete on fees. So what do you call the David seeking to unseat the Goliaths of financial services? How about AB401k?

![]()

| Features | AB401k | Typical Provider |

|---|---|---|

| ELIMINATE BROKERS | ABSOLUTELY | NOPE |

| ELIMINATE COMMISSIONS (12b1 FEES AND SUB-TA FEES) | YOU BET! | NEVER |

| ELIMINATE THE INCLUSION OF PROPRIETARY FUNDS | OF COURSE! | NO WAY |

| ELIMINATE KICKBACKS FROM THE FUNDS OFFERED | DARN RIGHT! | CHA-CHING! |

| LOW COST INDEX FUNDS | WE USE A CORE LIST OF LOW COST INDEX FUNDS (with no mark ups!) | INDEX FUNDS NOT OFFERED TO SMALL PLANS OR SOLD WITH HUGE MARK UPS ON FEES |

| FIDUCIARY PROTECTION FOR BUSINESS OWNER | INCLUDED | ALL LIABILITY REMAINS WITH BUSINESS OWNER |

| INVESTMENT ADVICE FOR PLAN PARTICIPANTS | "1-ON-1" ON-DEMAND ADVICE FOR PARTICIPANTS | EDUCATION ONLY |

| PLAN SERVICES | FULL SERVICE. INCLUDES ADMINISTRATION, RECORD KEEPING AND ADVISORY | UNBUNDLED. 3RD PARTY ADMINISTRATOR, 3RD PARTY RECORD-KEEPING, LOCAL BROKER, OUTSOURCED ADVISORY. |

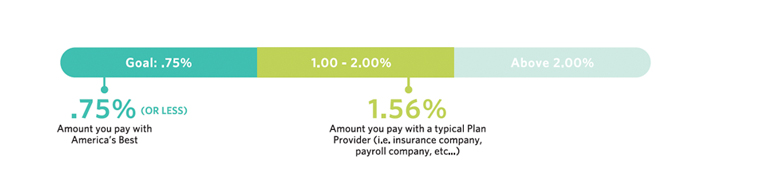

| FEES | 50-70% LESS ON AVERAGE. Click Here for Pricing | AVERAGE ANNUAL FEES OF 1.4% TO 2.5% |

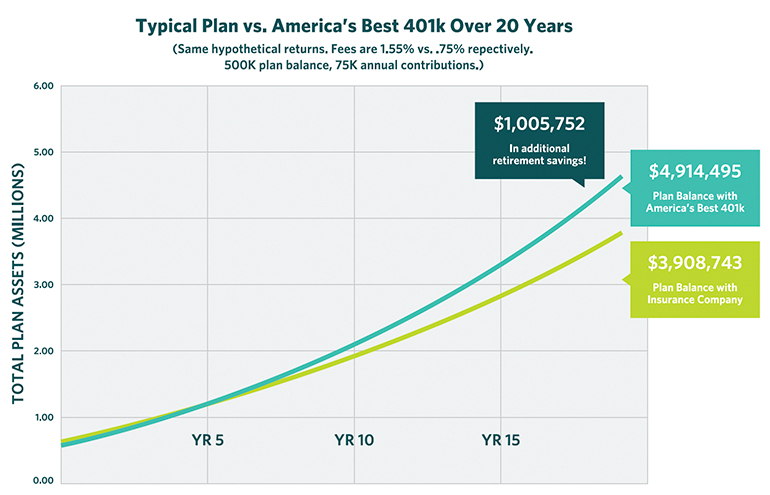

Imagine giving up 50% or more of your future nest-egg to excessive fees. Learn how to remove brokers and hefty commissions from your pocket.

Rarely do you see low cost index funds available in most plans. The typical plan is laden with expensive actively funds where the manager is sharing their fees with your provider. This arrangement directly impacts your returns.

The business owner (aka plan sponsor) is liable for their 401k choices! Increasingly, employees are suing employers for not taking the steps to eliminate excessive fees. The DOL is also out in full force in the matter.

A complimentary plan comparison will give you a look under the hood of your 401(k).

Get a free side by side comparison